Russia’s resurrected military industrial complex is cannibalising the rest of its economy

Ukraine is slowly losing the three-year conflict on the battlefield. Russia is slowly losing the economic conflict at a roughly equal pace. The Kremlin’s oil export revenues are too low to sustain a high-intensity war and nobody will lend Vladimir Putin a kopeck.

Russia’s overheated, military-Keynesian war economy looks much like the dysfunctional German war economy of late 1917, which had run out of skilled manpower and was holed below the waterline after three years of Allied blockade – as the logistical failures of the Ludendorff offensive would later reveal.

Putin’s strategic victory in Ukraine was far from inevitable a fortnight ago and it is less inevitable now after the Assad regime collapsed like a house of cards, shattering Putin’s credibility in the Middle East and the Sahel. He could do nothing to save his sole state ally in the Arab world.

“The limits of Russian military power have been revealed,” said Tim Ash, a regional expert at Bluebay Asset Management and a Chatham House fellow.

Turkey is now master of the region. Turkish forces had to step in to rescue stranded Russian generals. Even if Putin succeeds in holding on to his naval base at Tartus – a big if – this concession will be on Ottoman terms and sufferance. “Putin now goes into Ukraine peace talks from a position of weakness,” said Mr Ash.

When Trump won the US elections in 2016, corks of Golubitskoe Villa Romanov popped at the Kremlin. There were no illusions this time. Anton Barbashin from Riddle Russia says Donald Trump imposed 40 rounds of sanctions on Russia, belying his bonhomie with Putin before the cameras. He has since warned that Putin will not get all of the four annexed (but unconquered) oblasts of Donetsk, Luhansk, Kherson and Zaporizhia.

The Kremlin had banked on a contested election outcome in the US, followed by months of disarray that would discredit US democracy across the world. The polite interregnum has been a cruel disappointment.

Barbashin says Russia’s leaders expect Trump to issue ultimatums to both Kyiv and Moscow: if Volodymyr Zelensky balks at peace terms, the US will sever all military aid; if Putin drags his feet, the US will up the military ante and carpet-bomb the Russian economy.

That economy held up well for two years but this third year has become harder. The central bank has raised interest rates to 21pc to choke off an inflation spiral. “The economy cannot exist like this for long. It’s a colossal challenge for business and banks,” said German Gref, Sberbank’s chief executive.

Sergei Chemezov, head of the defence giant Rostec, said the monetary squeeze was becoming dangerous. “If we continue like this, most companies will essentially go bankrupt. At rates of more than 20pc, I don’t know of a single business that can make a profit, not even an arms trader,” he said.

The resurrection of the Soviet military industrial complex – to borrow a term from Pierre-Marie Meunier, the French intelligence analyst – is cannibalising the rest of the economy. Some 800,000 of the young and best-educated have left the country. The numbers slaughtered or maimed in the meat grinder are approaching half a million.

Russia’s digital minister says the shortage of IT workers is around 600,000. The defence industry has 400,000 unfilled positions. The total labour shortage is near 5m.

Anatoly Kovalev, head of Zelenograd Nanotechnology Centre, said his industry was crippled by lack of equipment and could not replace foreign supplies. “There is a shortage of qualified specialists: engineers, technologists, developers, designers. There are practically no colleges and technical schools that train personnel for the industry,” he said.

Total export earnings from all fossil fuels were running at about $1.2bn (£940m) a day in mid-2022. They have fallen for the last 10 months consecutively and are now barely $600mn. The Kremlin takes a slice of this for the budget but it is far too little to fund a war machine gobbling up a 10th of GDP in one way or another.

Oil tax revenues slumped to $5.8bn in November, based on a Urals price averaging near $65 a barrel. That price could fall a lot further. Russia is facing an incipient price war with Saudi Arabia in Asian markets.

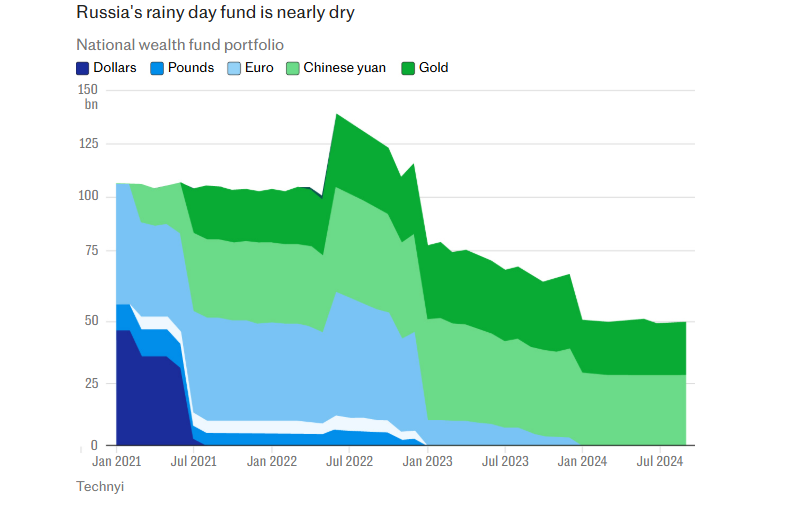

Putin is raiding the National Wealth Fund to cover the shortfall. Its liquid assets have fallen to a 16-year low of $54bn. Its gold reserves have dropped from 554 to 279 tonnes over the last 15 months. The fund is left with illiquid holdings that cannot be crystallised, such as an equity stake in Aeroflot.

The long-awaited rally in oil prices keeps refusing to happen. JP Morgan said excess global supply next year would reach 1.3m barrels a day due to rising output from Brazil, Guyana, and US shale. Rosneft’s Igor Sechin has told his old KGB friend Putin to brace for $45-$50 next year. Adjusted for inflation, that matches levels that bankrupted the Soviet Union in the 1980s.

The purpose of the G7’s convoluted oil sanctions was – until a month ago – to eat into Putin’s revenue without curtailing global oil supply and worsening the cost of living shock in the West. This has been a partial success. Russia had to assemble a shadow fleet of tankers and ship oil from Baltic and Black Sea ports to buyers in India and China, who pressed a hard bargain.

The International Energy Agency estimates that the discount on Urals crude has averaged $15 over 2023 to 2024, depriving Putin of $75m a day in export revenues.

Russia can get around technology sanctions but its systems are configured to western semiconductors. These chips cannot easily be replaced by Chinese suppliers, even if they were willing to risk US secondary sanctions, which most are not. The chips are bought at a stiff premium on the global black market and are unreliable.

Ukrainian troops have noticed that Russian Geran-2 drones keep spinning out of control. The Washington Post reports that laser-guided devices on Russia’s T-90M tanks have “mysteriously disappeared”, greatly reducing capability.

The industry ministry has been trying to develop analogues to replace chips from Texas Instruments, Aeroflex and Cypress but admitted in October that all three tenders had failed. Alexey Novoselov from the circuits company Milandr said Russia could not obtain the insulator technologies needed to make chips of 90 nanometers or below. It is the dark ages.

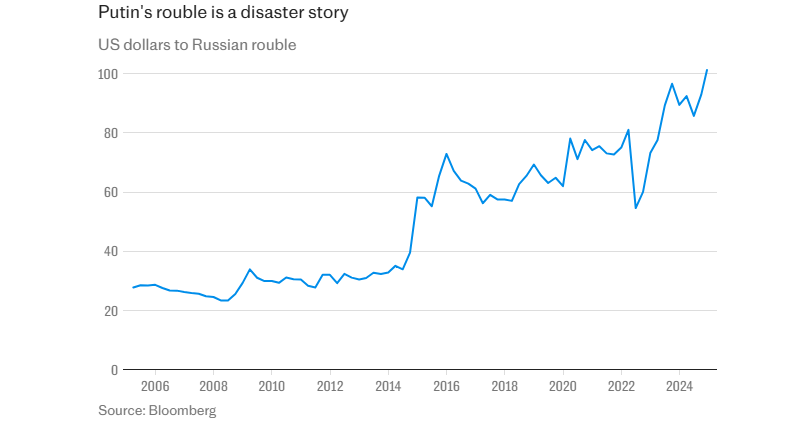

The US tightened the noose three weeks ago, imposing sanctions on Gazprombank and over 50 Russian banks linked to global transactions. This has greatly complicated Russia’s ability to trade energy and buy technology on the black market. It briefly crashed the ruble, now hovering at around 100 to the dollar.

Chinese banks have stopped accepting Russian UnionPay cards. The Chinese press says exporters have pulled back from Russian e-commerce sites such as Yandez or Wildberries because payment fees through third-parties no longer cover thin profit margins. Some have been unable to extract their money from Russia and are facing large losses.

Few foresaw the sudden and total collapse of the Soviet regime, though all the signs of economic decay and imperial overreach were there to see by 1989.

Putin’s regime is not yet at this point but it would only take one more change in the Middle East to bring matters to a head. If the Saudis again decide to flood the world with cheap crude to recoup market share – as many predict – oil will fall below $40 and Russia will spin out of economic control.

The Ukraine war may end in Riyadh.